Binance on Monday halted bitcoin withdrawals hours after crypto lender Celsius blocked customers from withdrawing funds from its platform in moves that prompted a widespread sell-off in the digital asset market.

Bitcoin, ether and other major tokens fell sharply on Monday after a volatile weekend as the market infrastructure that underpins the digital asset market showed signs of worsening stress. .

Binance, the world’s largest cryptocurrency exchange, suspended customer bitcoin withdrawals on Monday afternoon. The pause comes after Celsius, another major player in the crypto space that allows users to lend out their tokens for high returns, halted redemptions due to “extreme market conditions”. harsh”.

The crypto market has been rocked in recent weeks amid a broader flight from speculative assets as global central banks abruptly tightened monetary policy in response to intense inflation.

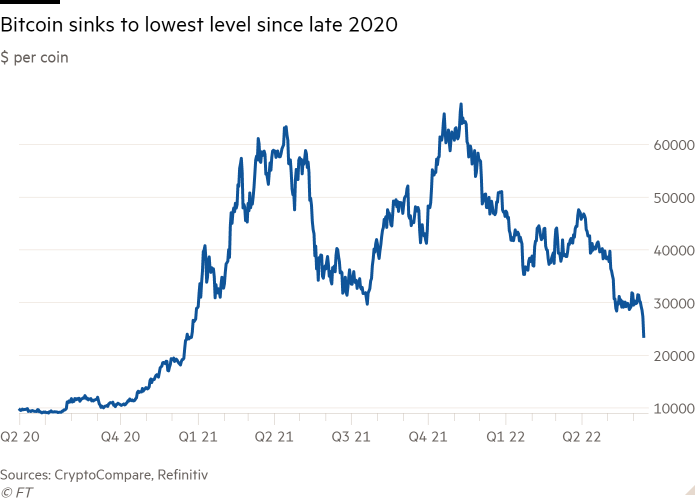

Bitcoin, the most actively traded in the world electronic money, has fallen nearly 20% since Friday to just under $24,000, its lowest level since December 2020, according to CryptoCompare data. Meanwhile, the broader crypto market’s market value has dropped from a peak of $3.2 billion in November to around $1 billion. in Monday.

Binance, the world’s largest cryptocurrency exchange by volume, said it has suspended bitcoin withdrawals from its platform due to “trading stuck”. The company, which processed $1.2 billion in crypto and derivatives trades last month, could not immediately provide details on the matter.

Celsius is one of the biggest players in the digital for-profit product market, offering users the ability to lend their tokens as collateral to other crypto projects. In return for lending their tokens, traders can earn an annual return of up to 17%.

Sentiment towards these high-risk projects cooled sharply after the terra and luna tokens – which are the foundation of another popular profit platform – collapsed over the next few days. Value of assets deposited on the Celsius platform fell below 12 billion dollars on May 17 from over $24 billion at the end of December.

Ether, seen as a proxy for sentiment towards digital asset projects that offer high returns to investors, has fallen nearly 30% since Friday, making it down two-thirds in coin dollars this year to trade at $1,195.

Monday’s sale also profited from shares of crypto-focused companies. MicroStrategy, a technology company that invests heavily in bitcoin, lost a quarter of its value in initial Wall Street trading while Nasdaq-listed Coinbase crypto exchange fell 16%.

Last year, Celsius raised $400 million in an equity funding round led by Caisse de Đépôt et setting du Québec, Canada’s second-largest pension fund, and WestCap, a fund run by former Airbnb executives and Blackstone Laurence Tosi, founded.

That fundraising comes even as US regulators say they are scrutinizing the industry. State authorities in Texas and New Jersey have alleged that Celsius’s profitable accounts amounted to an unregistered securities offering.

C’s early halt of withdrawals on Monday is also a turning point after it spent several days refuting allegations that customers were unable to make withdrawals. CEO Alex Mashinsky challenged critics over the weekend to find “even one person with a withdrawal problem”.

Celsius, which has offices in the US, UK and Lithuania, said the exchange freeze was in place “in the interest of our entire community to stabilize liquidity and operations while we take steps for the preservation and protection of property”.

The team’s own coin, known by its token CEL, has lost half its value in the past 24 hours, according to CryptoCompare data.