From Suffering to Recovering: The stats that explain why the UK music industry is set for a dramatic post-lockdown comeback.

The following MBW analysis comes from Will Page, author of Tarzan Economics: Eight Principles of Turning Through Disruption. Page (pictured) was formerly Chief Economist of Spotify and PRS For music.

‘Ships pass each other in the night’ is how I describe Britain’s live and recorded music industry in one Billboards article in the dark days of lockdown, June 2020.

Streaming has become a ‘home stock’, subscriber growth and streaming numbers. In contrast, live music has been silenced by the restrictions placed on our freedoms to contain the pandemic.

That paper provided an evidence base to help policymakers and contributors to the UK Government announces £1.6 billion funding package for the arts next month, and then the UK Government launched a £750 million insurance scheme for live events next year.

The important thing, as one Scottish Prime Minister has repeatedly told me, is ‘evidence-based policy making, not policy-based evidence-making’.

I am indebted to the UK PRS for musiclicenses live events so that its musician members can collect performance royalties when their songs are played at concerts.

Its data on the UK market, combined with data on music spending recorded by Entertainment Retailers Associationallows me to model consumer spending in times of crisis.

Now, they have let me update the analysis.

The exclusive insights gained from this work are astounding. Seatbelt.

Direct versus recorded music spending. (Does anyone remember 2019?)

Let’s go back to when the world was normal.

In 2019, UK showgoers spent £1.7 billion on concert tickets (or ‘box office’), one-fifth more than the £1.4 billion that consumers spent on the track recorded in the same 12 months.

In total, British music fans spent a total of £3.1 billion on music in 2019.

(Also: this concert spending captures only the primary ticketing market – what is often called ‘face value’ – and ignores the secondary markets and ancillary spending.)

Then the music was turned off from our stage, but played back on our phones.

In the surreal year of 2020, ‘box office receipts’ plunged 90% in the UK to just £200m – while spending on recorded music increased 6% to pass the £1.5bn mark.

As the lockdown eases into 2021, the streaming success continues, pushing UK spending on recorded music to almost £1.7 billion (ironically, the same value of the UK box office before the pandemic), while direct spending recouped some of its losses, grossing £700 million. office (still less than half of what it used to be).

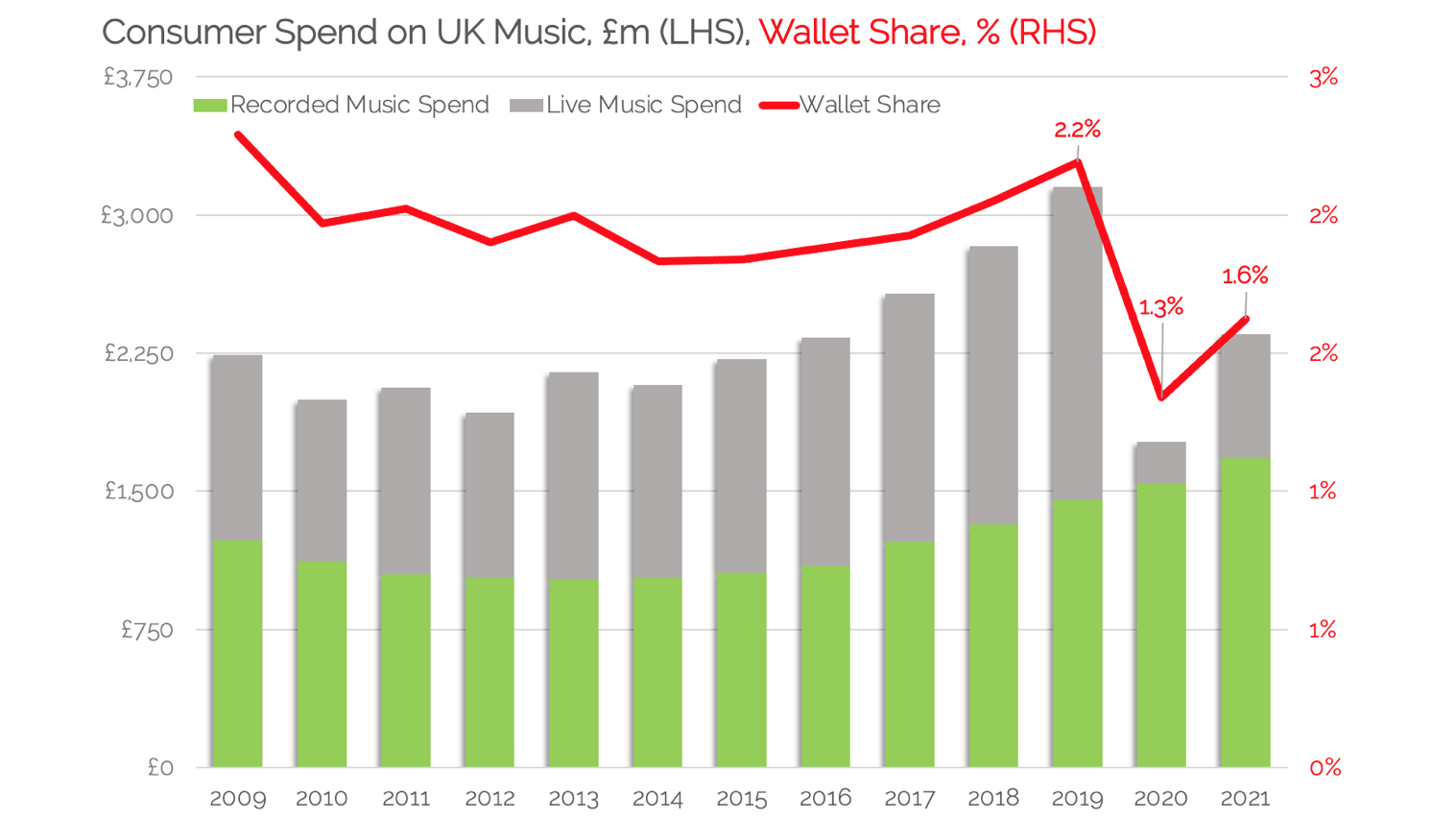

The importance of ‘share wallets’ – and how UK consumers spend 0.2% of their money on music

We can stack both components of the British music industry on top of each other and add one final piece of the puzzle: shared wallets.

Research team at Office for National Statistics studied the impact of Covid on consumer spending in the UK please provide me with data on entertainment and culture spending. This allows me to measure the UK’s total spending on music as part of what is commonly known as ‘entertainment dollars’.

Think about this for a small minute: a pound in every ten spent today in the UK is for pleasure and relaxation – but only two percent of that entertainment spending (that spending is just 0.2% in the grand total) is spent on live and recorded music.

Fart huh?

Now, let’s go to our chart.

On the left, recorded music spending is in green, stacked with box office spending in gray. On the right, the red line shows the share of entertainment spending.

The gin-and-tonic relationship of increasing subscriptions drives an increasing share of gig wallets from 2% next year 2015 2.2% in 2019 – a bigger market share in a bigger wallet.

When the account lockout occurs in 2020, the wallets are contracted and the wallet share rate drops 1.3% (share less with less money), recover to 1.6% last year.

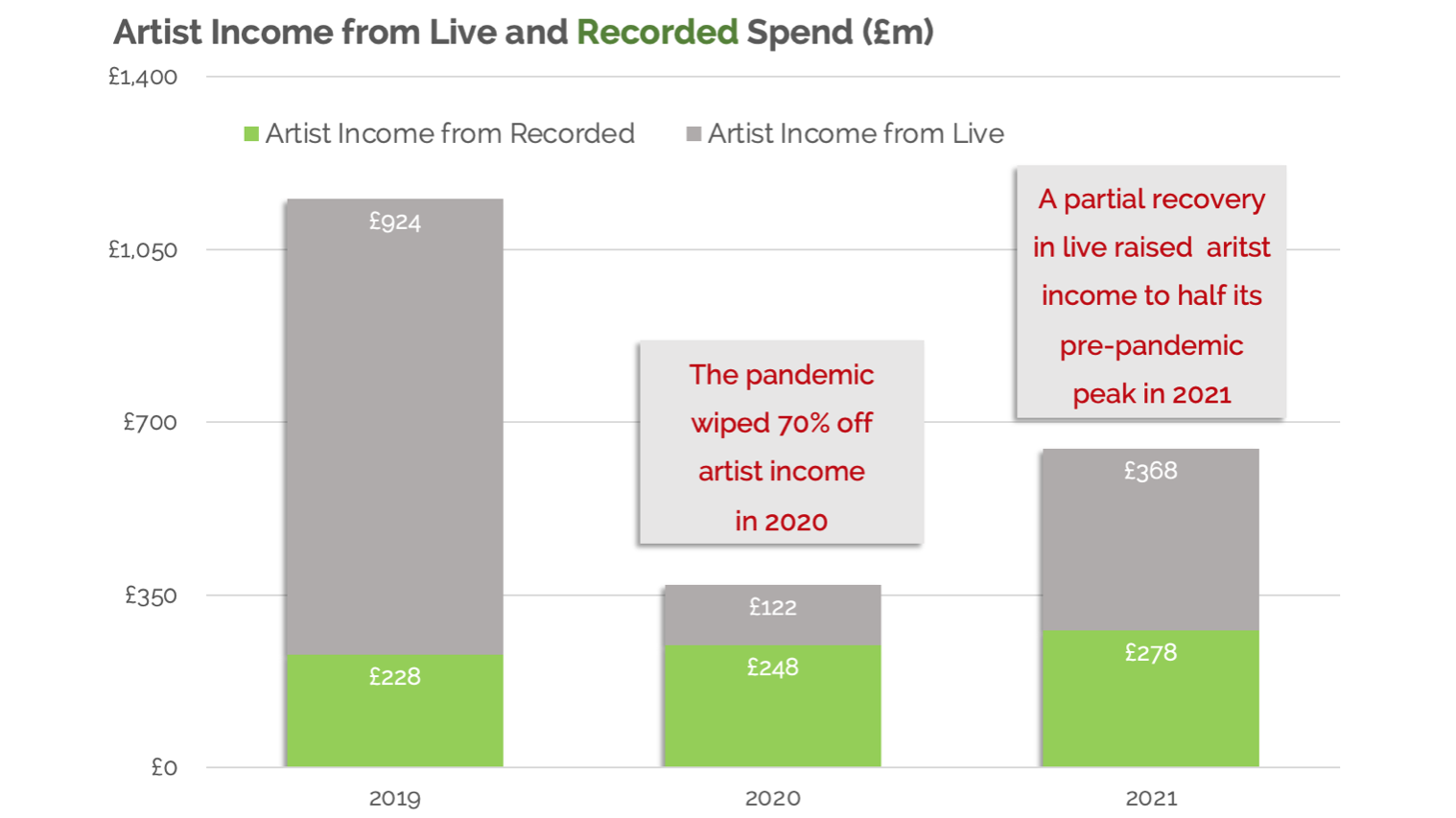

Now let’s find out what these lofty numbers mean to artists.

For live music, we remove fees and taxes from the face value of tickets and provide artists 75% what remains.

For recorded music, we take the wholesale value of genuine music and provide it to the artist 25%.

Curiously, these assumptions give a 80/20 Rules for 2019: 80% artist’s income comes from gigs and 20% from audio recordings.

Since live music is a mainstay for most artists, its silence in 2020 has eclipsed streaming growth, erasing 70% reduce their income.

If artists were struggling to make ends meet before we shut down the UK economy, they were 70% less to earn a living later.

And in 2021, a partial recovery in live streaming and continued growth in streaming has reduced artist earnings to half what they were before. For individual artists, (less so for companies), it’s really hard.

Although there is no such thing as ‘ordinary artist’, the average salary drops to 70% question of survival.

In 2019, live music income is larger (and distributed to a few) while recorded music income is smaller (and distributed among many).

The sudden pandemic changes that mix.

As streaming has more mouths to eat – and with nothing else to feed them – it’s no surprise that UK industry has weathered an arduous Parliamentary Inquiry throughout the years of stalemate.

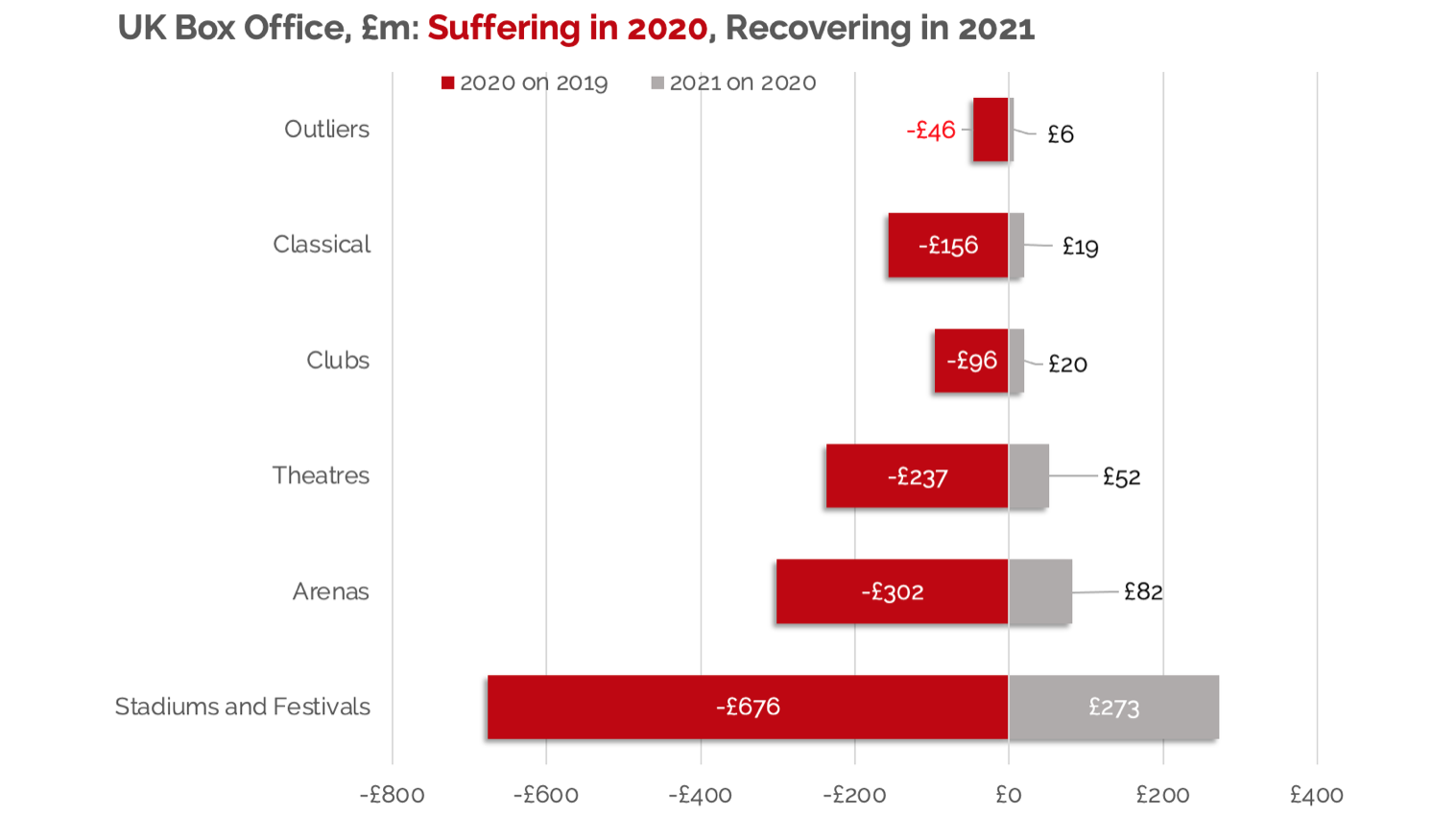

Now let’s focus on ‘suffering and healing’ in live music.

In one New Year’s essay I have shown that, since the London Olympics, all of the UK’s live music growth has been in stadiums and festivals – increasing their market share from 23% 2012 to 40% in 2019.

That is the price to pay for theatres, clubs and establishments having felt forced out of the UK market, in absolute and relative terms.

The chart below clearly illustrates that the harder it is to come: Stadiums and festivals cost more at the box office than arenas, theaters and clubs combined in 2020, reducing the market share of them at the UK box office down to just 10%.

From boom to boom to boom again, 2021 sees these outdoor events grow their box office revenue by more than a quarter of a billion dollars, lifting their box office share to record levels. 45%.

To use ‘long tail’ language, the UK living industry has never been so ‘affected’ – where the spoils are very few events.

Where do we go now?

These details, exclusively for Worldwide music businessraises questions that a global industry can learn from.

- The first day, How much is important? in recovery? Larger events owned by larger companies may be better able to comply with the moving target of government regulations.

- Second, will the travel restrictions help UK artists climb up the UK festival charts and if so, will it last?

- Third, we had two years at home ‘sofa inertia’ (that’s Netflix and Pringles for you and me) so what would happen for behaviors to change and get us off the sofa and back into the music venues?

To be sure, we’re still a long way from reaching our pre-pandemic peak with £3.2 billion in consumer spending and a 2.2% market share in wallets.

But going back to Gordon Brown’s view of evidence-based policy making (and not evidence-based policymaking), this work offers policymakers and experts in the foundation industry needed to find the support and action needed to get us back where we once belonged.

This will not be easy.

Wallets are set to be tightened further this year and next. That said, with the intertwined nature of the Parliamentary Inquiry behind us, it is imperative that all of us – policymakers, professionals and performers – get together. each other to address the need for a musical ‘roll spring’ on British and national stages.

James Taylor [not that one!] Listen to music for Wembley Stadium. He sees this spring roll in action: this summer, 16 record-breaking concerts are taking place at the famed stadium with a staggering 1.3 million tickets sold; It’s a population of Edinburgh and Glasgowcombine!

Now that the dust has settled, let’s remind ourselves that music is the alchemy of the room that brings us together. And with the final pandemic behind us, those rooms are bound to fill up to capacity.

If the ‘us’ collective gets it right, it will feel more like a slingshot than a rebound.

Authors thank: John Mottram and Frances Hodgson (PRSforMusic); Katherine Kent and Luke Croydon (Office for National Statistics), Liz Martins (HSBC Economics), Tim Chambers, Bill Gorjance, Ralph Simon, Association of Leisure Retailers and BPI.

I also want to say thank you to DICE for their comprehensive data on the UK live events industry.

Page will Tarzan Economics: Eight Principles of Turning Through Disruption (pictured) has now been released through Simon & Schuster (UK) and Little, Brown and Company (USA).Worldwide music business